Exploring the impact of the EU sustainability reporting landscape on companies in Asia

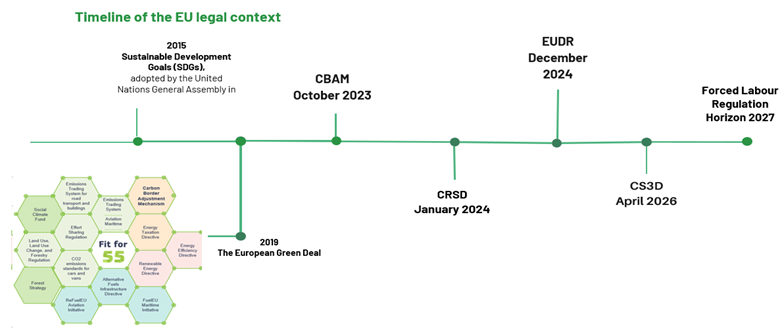

The European Union (“EU”) has been a driving force in environmental, social and governance (“ESG”) regulations. The EU’s environmental policies are part of a broader commitment to the Sustainable Development Goals (“SDGs”), adopted by the United Nations General Assembly[1] in 2015. These goals address critical global challenges such as climate change, environmental degradation, and social inequality.

In 2019, the EU announced the European Green Deal, setting an ambitious target of achieving zero net greenhouse gas (“GHG”) emissions by 2050. This initiative underscores the EU’s dedication to becoming the world’s first climate-neutral continent.

To support this goal, the EU has implemented a series of regulatory measures designed to promote sustainability and mitigate the impacts of climate change, including:

- the Directive 2022/2464 on corporate sustainability reporting (“CRSD”),

- the Regulation (EU) 2023/1115 on the making available on the Union market and the export from the Union of certain commodities and products associated with deforestation and forest degradation (“EUDR”),

- the Regulation (EU) 2023/956 establishing a carbon border adjustment mechanism (“CBAM”),

- the proposed Regulation (EU) on prohibiting products made with forced labour on the Union market (“Forced Labor Regulation”).

Together, these initiatives seek to drive a more sustainable economy by ensuring that companies adhere to stringent environmental standards and provide clear, reliable information to investors and consumers.

While these regulations are EU-driven, their impact extends globally. Companies worldwide that wish to do business in the EU or with EU-based companies must adapt to these standards. This requirement to adopt the EU standards has a cascading effect, pushing global supply chains towards greater sustainability and ethical practices.

The ASEAN Taxonomy Board (“ATB”), set up under the auspices of the ASEAN Finance Ministers and Central Bank Governors’ Meeting also participates to the creation of ESG guidelines by developing, maintaining and promoting a multi-tiered guide on ASEAN Taxonomy for Sustainable Finance (“ASEAN Taxonomy”) which identifies economic activities that are sustainable and help direct investment and funding towards a sustainable ASEAN.

The ASEAN Taxonomy (Version 3 published on 27 March 2024) is an overarching guide for all ASEAN Member States (“AMS”), complementing their respective national sustainability initiatives and serving as ASEAN’s common language for sustainable finance. It is designed to ensure that AMS have a framework that suits their economic and social structures that other frameworks may not be able to address.

In this newsletter, we aim to provide:

- a better understanding of the EU’s sustainability reporting landscape;

- how it compares to five key Asian jurisdictions: China, Indonesia, India, Vietnam and Singapore; and

- steps to take to comply with the new EU regulations.

I. Understanding the EU’s sustainability reporting landscape

1. Key definitions and timeline

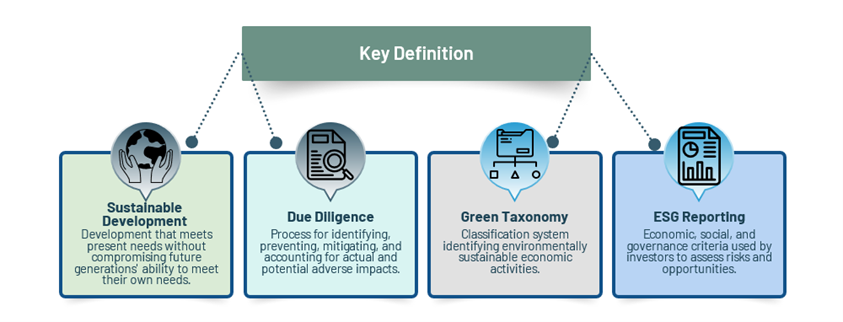

A. Key Definitions

2. Timeline of the EU legal context

3. CSRD

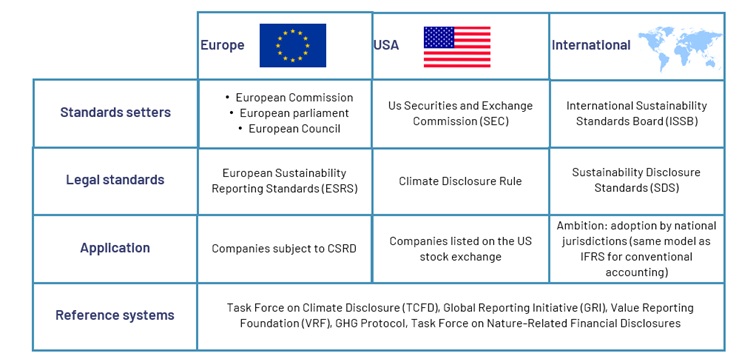

The CSRD is a critical part of the EU’s environmental strategy. It replaces Directive 2014/95 on disclosure of non-financial and diversity information by certain large undertakings and groups (“NFRD”) and aims to enhance the reliability and accessibility of sustainability information through standardized and comprehensive reporting. Since 1st January 2024, the CSRD mandates companies that meet certain thresholds to report on Environmental, Social, and Governance (ESG) criteria, integrating sustainable finance and green taxonomy principles. It introduces the concept of “dual materiality,” ensuring that companies report on how sustainability issues affect them and their impact on society and the environment. This standardized reporting aims to improve the reliability and transparency of sustainability data, guiding investors, and stakeholders towards more informed decisions.

A. Comparison with other international initiatives

In comparison with the other international regulations, the CSRD can be considered as the most ambitious of the ESG information standardisation initiatives.

B. Scope of application and road map

CSRD will be implemented in phases as illustrated below:

| Large Public Interest Entities (PIEs) with >500 Employees (Already Subject to NFRD): | Large Companies Newly Subject to CSRD (Including Large Listed Companies with < 500 Employees): | Listed Small and Medium-Sized Enterprises (SMEs): | Non-European Companies Meeting CSRD Conditions: |

| 2024 – Immediate Action: Begin preparing for CSRD compliance based on cross-sector standards. | 2024/2025 – Preparation Phase: Prepare for CSRD compliance based on cross-sector standards. | 2026/2028 – Preparation and Transition Phase : Prepare for CSRD compliance based on specific ESRS standards. | 2028-Preparation Phase : Prepare for CSRD compliance based on specific ESRS standards. |

| Key Steps: Assess current sustainability reporting and identify gaps.Update internal processes for data collection and reporting.Allocate resources and designate teams for CSRD compliance.Engage with stakeholders to understand their expectations.Conduct a materiality analysis to identify key sustainability issues. Outcomes: Establish a CSRD compliance framework.Initiate data gathering and reporting activities. | Key Steps: Familiarize with CSRD requirements and guidelines.Conduct a gap analysis comparing current practices with CSRD requirements.Develop a roadmap and timeline for CSRD implementation.Enhance internal capacity for sustainability reporting.Consider engaging external experts for support. Outcomes: Gain a clear understanding of CSRD obligations.Begin internal preparations for compliance. | Key Steps: Monitor developments in ESRS standards and guidelines.Evaluate readiness for sustainability reporting.Implement changes to internal processes and systems.Train and support relevant staff members.Develop a communication strategy for stakeholder engagement. Outcomes: Align internal systems with CSRD requirements.Begin sustainability reporting activities | Key Steps: Understand CSRD requirements and implications for non-European companies.Assess operations and supply chains comprehensively.Collaborate with European subsidiaries or partners for data gathering.Develop strategies to address compliance challenges.Establish communication channels with regulatory authorities for guidance. Outcomes: Develop a CSRD compliance plan.Initiate necessary actions to meet requirements. |

C. Controls and penalties:

Statutory auditor or audit form must carry out the assurance of sustainability reporting. As most of the European regulations, each member state must ensure that the provisions of the directive are implemented by providing an effective, proportionate, and dissuasive sanction to auditors and audit firms.

3. CBAM

The CBAM aims to prevent carbon leakage by ensuring equivalent carbon pricing for imports and EU products. It gradually phases out free allowances under the EU Emissions Trading System (ETS) and introduces a carbon pricing mechanism for imports, ensuring that non-EU products are not favored over EU products. This mechanism supports the goal of climate neutrality and aligns with international climate commitments, such as the Glasgow Climate Pact and the Paris Agreement. These regulations aim to reduce the EU’s carbon footprint and promote sustainable economic activities that do not exacerbate climate change.

A. Scope of application:

The CBAM creates new regulatory obligations for importers and will initially apply only to the following sectors: cement, aluminum, nitrogen fertilizers, electricity and hydrogen.

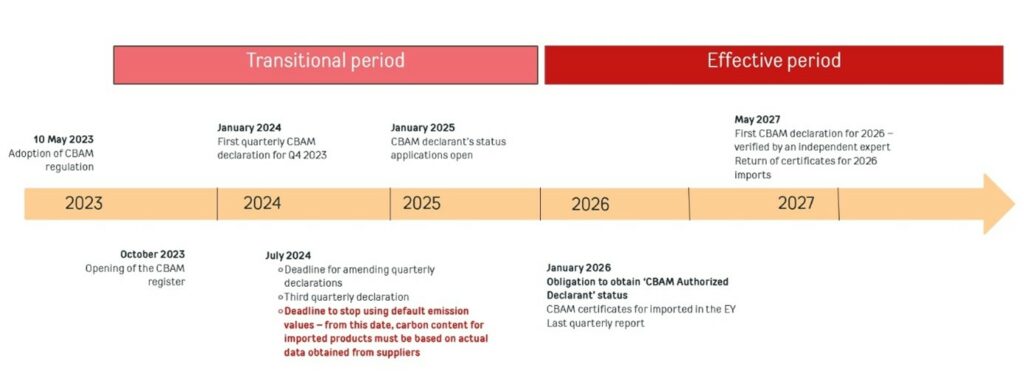

The CBAM places the main liability on the EU importer, however the regulatory obligations will require concerns all economic operators and strong cooperation between producers or suppliers and buyers involved in the supply chain concerned in international trade from or to of products imported in the EU. The CBAM provides a transition phase and an effective operating period:

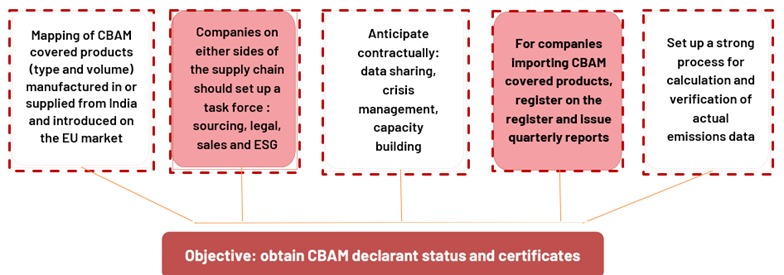

B. Obligations under CBAM

First, every importer of products covered by CBAM has to register on the CBAM register and issue quarterly reports until January 2026. Until this date, every importer will have to apply for authorized declarant status. Starting 2026, imports of CBAM products will need to be made with a CBAM certificate, whose price will be related to the carbon emissions embedded in the products imported, as calculated by the producer/supplier. From 2026, before 31st May of each year, authorized CBAM declarants will issue the CBAM register to submit a CBAM declaration for the previous calendar year.

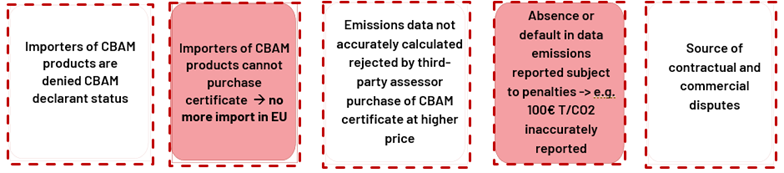

C. Effects of non-compliance

4. EUDR

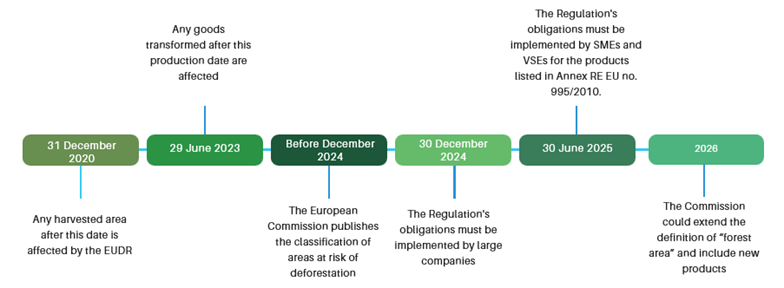

The EUDR aims to tackle global deforestation, a major contributor to climate change and biodiversity loss and imposes strict rules in terms of due diligence to all companies wishing to market affected products in the EU or to export them. The EUDR is part of the EU’s broader strategy to protect biodiversity, as reflected in its commitments under the Convention on Biological Diversity (CBD) and the European Green Deal. Companies have until 30 December 2024 to be compliant, except for micro and small undertakings for which the EUDR will apply from 30 June 2025.

A. Scope of application

The products concerned by the EUDR are those from the following sectors: cattle, rubber, wood, soya, cocoa, coffee and palm oil. They will only be authorised to be placed on the EU market or exported if they are deforestation-free, produced in accordance with relevant local legislation and covered by a due diligence statement. Any of those product’s export to the EU, found in the food, luxury or automobile industry, in any level of the value chain (not only raw product) are concerned except if they fall into the category of recycled basic and used products that would otherwise be disposed of as waste.

To prevent and dissuade potential deforestation resulting from anticipated acceleration in the activities causing deforestation, any production activity occurring after the 31 December 2020 will be affected. Concerning the transformed goods, this regulation will apply to any products for which the production date is prior to the 29 of June 2023 and 30 December 2024 for wood.

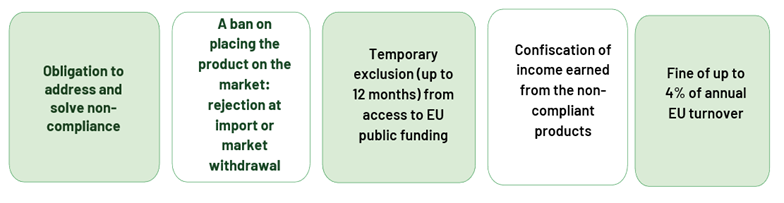

B. Corrective measure and penalties

In case of non-compliance, companies will have to address and solve the non-compliance and may face the following sanctions:

5. Forced Labor regulation

The Forced Labour Regulation aims at preventing products made with forced labor from entering the EU market, prohibiting the import of goods produced using forced labor, requiring companies to ensure their supply chains are free from forced labor and to provide transparency about their sourcing practices, and establishing mechanisms for monitoring and enforcing compliance, including inspections and penalties for violators. The Forced Labour Regulation goal is to combat forced labor globally by leveraging the EU’s market power to encourage ethical labor practices.

A. Scope of application

This regulation will apply to all products entering into the EU market and all parties (economic operator, producer, supplier, importer, etc.) on the supply chain are concerned.

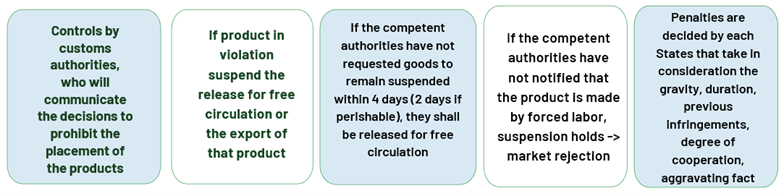

B. Controls and sanctions

Compliance with the Forced Albor Regulations will be monitored by customs authorities and non-compliance will have the following consequences:

This new EU sustainability reporting landscape is part of a broader effort to promote sustainable development and address global environmental challenges, including in Asia. For several years, Asia has been undergoing significant developments: many nations have implemented their own environmental regulations, reflecting varying levels of commitment and approaches to sustainability.

But how is Asia EU-ESG ready and how will the EU regulations impact companies in China, Indonesia, India, Vietnam and India?

China

In China, the concept of ESG originated abroad but has gained momentum due to its alignment with the imperative of green economic development and social equity. This commitment was reinforced in 2020 when Chinese President Xi Jinping delivered a landmark address at the 75th United Nations General Assembly, pledging to achieve carbon peak by 2030 and carbon neutrality by 2060, encapsulating the ambitious ‘dual carbon’ goal. Furthermore, the report to the 20th National Congress of the Communist Party of China stressed the importance of promoting common prosperity for the sake of social equity.

Below, we delve into the ESG regulatory framework in China.

1. Environment

China has established a relatively comprehensive legal system in the field of environmental protection, covering various aspects such as air, water, soil, solid waste, and noise pollution prevention. These laws and regulations provide environmental standards and requirements for enterprises and offer enforcement bases for government departments.

The recent National Plan for Ecological Conservation and Green Development issued by the State Council in 2023 sets forth a strategic roadmap for ecological conservation, the promotion of green industries, and comprehensive environmental governance. This plan outlines long-term goals for protecting biodiversity and natural habitats through targeted conservation projects, supporting industries that focus on sustainable practices, and strengthening regulatory frameworks to ensure effective environmental protection.

The Environmental Protection Law (revised in 2015) is a foundational legislation in China’s environmental protection domain, encompassing basic principles and systems for environmental protection. This legislation introduces stricter pollution control measures, including daily fines for violators, which serve as a financial deterrent to ensure compliance. Corporate executives are held accountable for environmental damages, with potential personal penalties and criminal charges for severe violations. This enforcement mechanism aims to reinforce a culture of responsibility at the highest levels of corporate governance.

In response to climate change and carbon emissions, China has implemented the “dual carbon” strategy, aiming to peak carbon emissions by 2030 and achieve carbon neutrality by 2060. Numerous policies, plans, and standards, including the Registration Management Rules for Carbon Emissions Rights, Trading Management Rules for Carbon Emissions Rights, and Settlement Management Rules for Carbon Emissions Rights, have been introduced to support this strategic goal, reflecting China’s commitment to addressing climate change. The establishment of a national carbon emission trading system in 2021 represents a significant step in China’s commitment to carbon reduction and climate action. This system regulates carbon emissions through a cap-and-trade mechanism, with detailed regulations on emission allowance allocation and trading mechanisms, ensuring a fair and transparent process for market-based emissions reductions.

China has also many departmental regulations, industry regulations, and standards governing environmental protection across various industries. Notable examples include the Cleaner Production Promotion Law, the Air Pollution Prevention and Control Law, and the Water Pollution Prevention and Control Law.

Regarding environmental information disclosure, the Measures for the Administration of the Legal Disclosure of Environmental Information by Enterprises, enacted by the Ministry of Ecology and Environment (MEE) in 2022, mandate that qualifying high-polluting enterprises, companies undergoing clean production audits, listed companies, and bond-issuing entities with a history of environmental violations must disclose environmental information. Compliance with the Guidelines on the Format for the Legal Disclosure of Environmental Information by Enterprises, concurrently issued by the MEE in 2022, is compulsory when preparing such disclosure reports.

The Guidelines on Investor Relations Management of Listed Companies, published by the China Securities Regulatory Commission (CSRC) in 2022, explicitly direct listed firms to share ESG information, particularly environmental information, with investors. Consistent with this directive, Chinese stock exchanges have actively promoted ESG disclosure frameworks, playing a vital role in advancing green finance and facilitating the listing of environmentally conscious businesses. Notably, the Shanghai Stock Exchange mandated all listed companies to disclose significant environmental incidents or events that could negatively impact their social responsibility standing, a requirement already applicable to companies listed on the STAR Market since 2019. Furthermore, effective May 1, 2024, China’s three major stock exchanges—Shanghai Stock Exchange (SSE), Shenzhen Stock Exchange (SZSE), and Beijing Stock Exchange (BSE)—introduce mandatory corporate sustainability disclosure requirements for certain listed companies such as constituents of the SSE 180 Index, the STAR 50 Index, and firms listed both domestically and internationally. These guidelines will reinforce the obligation for listed companies to disclose comprehensive ESG details, particularly environmental information, enhancing transparency and aligning with international ESG reporting standards.

Despite the relatively comprehensive legal framework on the environment as described above, China still faces challenges in advancing the environmental domain of ESG. For example, transparency and reliability of ESG data are one of the issues, with some companies providing incomplete or inaccurate information, complicating investors’ efforts to evaluate true environmental performance. Moreover, despite the existence of numerous environmental regulations, enforcement sometimes remains inconsistent as local governments may prioritize economic growth over strict compliance with environmental laws. Also, rapid industrialization and urbanization have exacerbated pollution problems, including air, water, and soil contamination, adversely affecting public health and ecosystems. Lastly, public awareness and participation in environmental protection are growing but remain limited. Addressing these issues requires strengthened regulatory enforcement, improved data transparency, and heightened environmental awareness among the public and businesses.

2. Social

In China, while no single, comprehensive legislation directly targets ESG’s social aspects, a constellation of laws and regulations address various elements pertinent to the social dimension of ESG. These laws emphasize positive societal impact management and corporate social responsibility.

Key areas covered include labor laws and social security regulations. The PRC Labor Law, PRC Labor Contract Law, and PRC Social Insurance Law are fundamental in safeguarding workers’ rights, dictating working hours, rest periods, wage payments, social security provisions, and occupational safety and health.

Additionally, fair business practices are promoted through the Chinese Antimonopoly Law and the Chinese Consumer Rights Protection Law, which ensure fair market competition and consumer protection.

Human rights protection is another crucial aspect upheld by the Chinese Constitution and associated laws that ensure fundamental human rights such as equality, labor rights, rest, and education. Specifically regarding forced labor regulation, China, as a founding member of the International Labour Organization (ILO), adheres to a legal infrastructure aimed at eradicating forced labor. The Chinese Constitution, particularly Article 37, safeguards personal liberty. This is echoed by the Chinese Labor Law and Chinese Labor Contract Law, which forbid employer coercion and allow employees to terminate contracts if subjected to such infringements. The Chinese Criminal Law penalizes forced labor, with offending corporations facing fines and executive accountability. Supplementary regulations scattered throughout other legal frameworks reinforce these provisions, such as Article 40 of the Public Security Administration Punishment Law, Article 6 of the Employment Promotion Law, and Article 6 of the Regulations on Paid Annual Leave for Employees. Notably, China ratified the 1930 Forced Labour Convention and the 1957 Abolition of Forced Labour Convention in April 2022, integrating international standards into domestic law and underscoring its commitment to workers’ rights and the eradication of forced labor.

Despite the relatively comprehensive legal frameworks, inconsistencies in enforcement and implementation may exist, particularly at the local level. Issues such as excessive overtime work, wage arrears, and inadequate enforcement of labor inspection systems are often highlighted as areas needing improvement. Conversely, while community engagement is not legally mandated, there is a growing trend among Chinese firms to engage in philanthropic activities and community development projects. This trend reflects an increasing recognition of the importance of maintaining a social license to operate.

3. Governance

The Chinese Company Law, updated in 2023, serves as the cornerstone of corporate governance in China. This law outlines the fundamental structure and operational rules for companies, including the establishment and functioning of shareholders’ meetings, boards of directors, and supervisory boards. By specifying the rights and duties of these governing bodies, the law ensures a balanced decision-making process. It also regulates shareholder rights, equity transfers, and dividend distributions, promoting transparency and fairness within companies.

The Guidelines for Listed Companies’ Governance, issued by the China Securities Regulatory Commission (CSRC) and updated in 2018, specifically target listed companies to enhance their governance practices. These guidelines mandate that at least one-third of the board members must be independent directors, a measure designed to protect minority shareholders’ interests. They emphasize transparency in information disclosure, robust risk management, and effective internal control systems, aligning Chinese corporate governance with international best practices.

The Anti-Unfair Competition Law, updated in 2019, aims to prevent unfair business practices such as commercial bribery, misleading advertising, and trade secret violations. By promoting fair competition, it ensures that companies adhere to ethical standards, which is a critical aspect of good corporate governance.

China’s Corporate Social Credit System (CSCS), officially outlined in the State Council’s “Planning Outline for the Construction of a Social Credit System (2014-2020)” released in June 2014, is not a single law but a comprehensive policy initiative that assesses companies based on their compliance with various laws, social responsibilities, and ethical standards. Companies with good credit records benefit from easier access to financing and other incentives, while those with poor performance face penalties and restrictions. The CSCS indirectly influences corporate governance by incentivizing ethical behavior and compliance, thereby promoting a culture of accountability.

Despite this legal framework, several challenges persist in practice and implementation. For example, while the Securities Law and the Guidelines for Listed Companies’ Governance require timely, complete, and accurate information disclosure, many companies fall short. Corruption and bribery are also ongoing issues.

Impact of EU regulations on companies in Asia

The implementation of ESG principles and compliance with regulations can have a significant impact on companies operating in or trading with the EU. Companies must adapt to new standards and practices to maintain market access and competitiveness. This includes integrating sustainability goals into their operations, investing in cleaner technologies, and ensuring compliance with environmental and social regulations.

The CSRD will require subsidiaries of European companies or companies within the value chain of European partners to initiate data collection and sustainability report compilation to provide to their European partners or parent companies upon request.

Subsidiaries of European companies will benefit from available resources and a sustainability strategy that has been cascaded from the parent company whereas companies within the value chain of European businesses will need to carry out more preparatory work to meet requirements from their European partners to comply with the CSRD as they may lack guidance on European regulations. It is therefore paramount that companies educate themselves and seek guidance from their European partners to assess actions to be taken at their level to initiate data collection and sustainability report compilation.

Although the implementation of the CBAM by the EU directly impacts key industries, exporters must navigate the evolving scope of CBAM, which may expand to include indirect emissions and additional carbon-intensive sectors. To remain competitive in the EU and minimize the impact on production and export activities, exporters are urged to monitor CBAM progress closely, study reporting requirements for greenhouse gas emissions, assess financial implications, evaluate commercial opportunities for greener products, and implement decarbonization policies and greener production methods.

In addition to CBAM, exporters must comply with EU regulations on forced labor and deforestation to access the European market. The forced labor products ban requires rigorous due diligence to ensure no forced labor risks exist in the supply chain, including online sales. Similarly, exporters must provide evidence that their products have not contributed to deforestation or forest degradation. Exporters face the challenge of increased effort in tracking and tracing the origins of export goods, requiring training for all participants in the supply chain.

Companies that succeed in adapting to these changes can enhance their reputation and competitiveness in the global market. However, those that do not comply may face barriers to market entry and potential financial sanctions. The emphasis on sustainability and responsible business practices should drive innovation and create new opportunities for proactive companies facing environmental and social challenges.

ux.